07350015%2E2014%2E948724

Teks penuh

Gambar

Garis besar

Dokumen terkait

Would this be enough to guarantee that the stan- dard parametric bootstrap method is valid for both the testing and the interval estimation for those parameters, avoiding

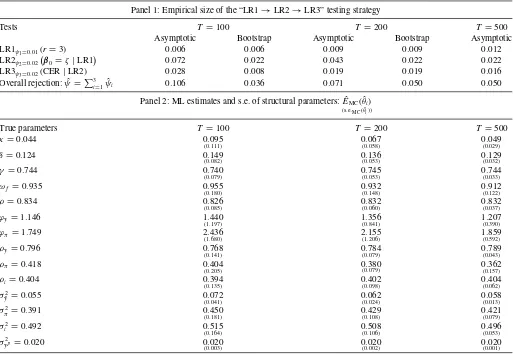

A set of simulation experiments was designed to uncover the size and power properties of bootstrap tests based on our proposed family of statistics, and to compare these properties

Since we use pairwise moment conditions in the trivariate cases, we restrict our attention to tests with at least two moment conditions. Our simulation results for the bivariate

An interesting implication of closely related work in Clark and McCracken (2012) is that even when one is testing the null hypothesis of equal MSPEs of forecasts from nested models

I completely concur, and I further suggest that, fundamentally, the biggest distinction between the many tests that have been proposed in the last 20 years is not the shape of

However, out-of-sample tests are no panacea in this regard— the extent to which out-of-sample forecasting results are more reliable than in-sample forecasting results depends on the

Our main finding is that the information contained in the covariates is useful when testing for a unit root in panel data, and that the power of the PCADF test can be

Herein, we define a nontrivial block Toeplitz matrix in the vein of Pe˜na and Rodr´ıguez ( 2002 ) and Mahdi and McLeod ( 2012 ) for use in the setting of testing for independence