Directory UMM :Data Elmu:jurnal:E:Economics Letters:Vol71.Issue1.Apr2001:

Teks penuh

Gambar

Dokumen terkait

Sibbesen (1986) subsequently used the model to simulate tillage derived soil and substance dispersion in 21 more than 50-year old ®eld experiments and estimated the mean content

The results of a Monte Carlo experiment show that imposing the curvature conditions on a system of demand equations improves the MSEs on estimated elasticities from 3 to 50%

Constant V* is estimated as the mean of M2 over the period from 1960:1 to 1988:4; Estimate A allows for a one-time shift in the intercept; Estimate B allows for a time trend and

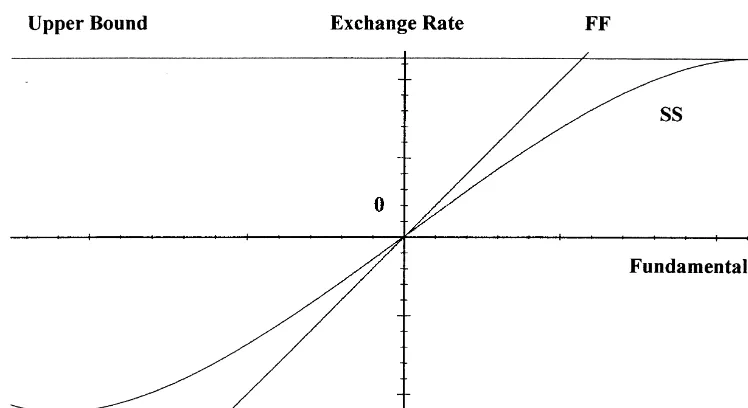

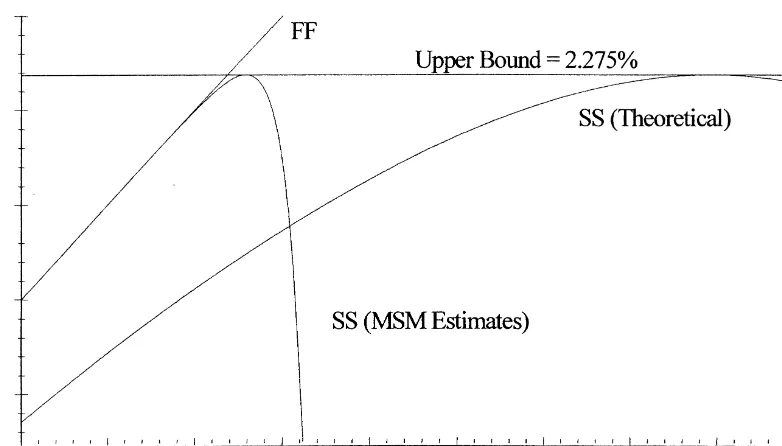

Moreover, our adjusted tests are designed for locally misspeci " ed alternatives close to q " o " 0.0, and the main objective of our Monte Carlo study is to investigate

Our simulations of a fractionally integrated stochastic volatility model, calibrated to the high-frequency returns, demonstrate that downward bias in the semiparametric estimates of

This paper has attempted to show the practicality and usefulness of the Bayesian approach, used in conjunction with Markov chain Monte Carlo methods, for the estimation of

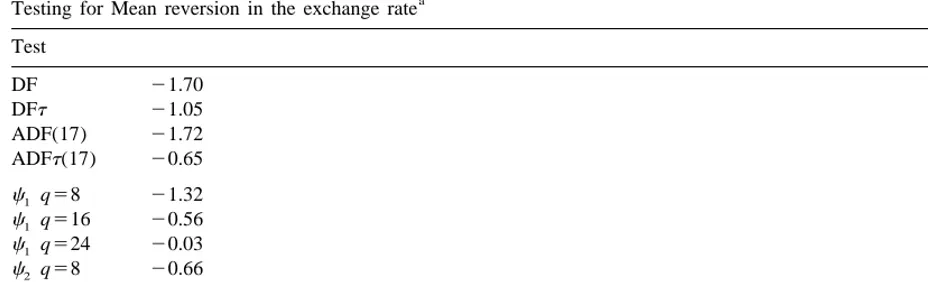

Out of the thirteen bilateral exchange rates, evidence of PPP is found for only one (the Mexican peso/U.S. dollar rate) under traditional tests for unit roots, while seven of

The purpose of this paper is to compare, through Monte Carlo methods, the power properties of three simple tests for the seasonal differencing filter when the data